Copper demand outlook no bright spot processing fee game or key in the fourth quarter

Hot spot funds flow to thousands of stocks to evaluate stocks to diagnose the latest rating simulation transaction

Client

Article source: WeChat public number information

Copper variety: report key logic

1. Demand logic outlook:

Globally, there is no over-emphasis on the overall demand, and the demand is generally growing at a slower rate, and the overall demand is changing slowly. Although the demand in the fourth quarter is a traditional peak season, the tracking situation from the national grid shows that it is difficult to change much.

2. Supply logic outlook:

The issue of new smelting capacity was put in the fourth quarter, but the copper negotiation team has set a higher threshold for processing fee procurement, so the increase in smelting capacity may not lead to an increase in supply.

Looking ahead, the tracking situation in September shows that the release of copper mine capacity in Chile and Peru will not be too strong, and there is still no pressure on the supply side in the medium and long term.

3. Supply and demand logic results:

On the whole, although the overall demand growth rate of copper is relatively low, and there is no obvious bright spot in the short term; however, from the supply point of view, before 2021, the growth rate of copper supply is relatively controllable, and the supply is released in an orderly manner. The long-term optimistic logic base still exists; therefore, the fourth quarter is still dominated by bargain hunting strategies.

Copper Variety: Strategy for the Fourth Quarter of 2017

1. Copper direction in the fourth quarter of 2017: wide fluctuations

2. Estimated shock range: below support yuan / ton

3. Suggestions for the fourth quarter of 2017: Concussion ideas, focusing on low-suction opportunities

Copper Variety: Strategic Risks for the Fourth Quarter of 2017

1. The concentrated release of refining capacity has led to a sharp narrowing of processing fees, and smelting companies have been forced to reduce operating rates.

2. Unexpected demand

3. Copper mine supply exceeded expectations

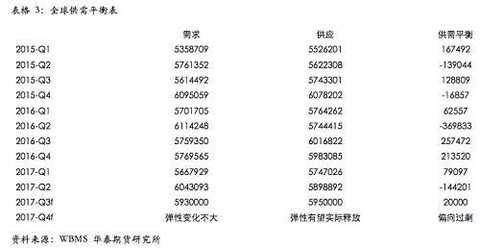

Supply and demand balance forecast

Global supply and demand balance:

The global supply mainly depends on the release of China's smelting capacity, and the elasticity of copper has been almost released.

|

China's supply and demand balance:

The overall demand change is not expected to be large. The bottom line of processing fees in the fourth quarter of China is relatively high, and the release of refined production capacity may not lead to an increase in supply.

|

Global copper supply and demand balance

Global supply and demand status of refined copper:

In the third quarter of 2017, overall demand maintained a moderate growth year-on-year, while supply resumed from the strike in Chile in the second quarter. It is expected that overall demand changes may not be large in the fourth quarter, while supply is subject to certain uncertainties, mainly due to the release of refined capacity. Does not necessarily lead to an increase in supply. And if the supply is released, or if you want to do more.

|

|

Global copper concentrate supply changes towards the future:

Production and expansion plans of the top ten copper concentrate enterprises:

In the third quarter, we adjusted the 2017 production forecast for the world's top ten copper concentrate companies based on company reports and media reports. In September, the production in FY2017 was stable compared to the previous period. However, with the release of unfavorable factors in the second half of the year, the expected production in FY18 has a certain elastic increase.

|

In September, Chile's National Copper Company (Codelco) said that the company's copper production in the first half of 2017 was lower than the same period last year, but the profit was considerable, due to the sharp rise in copper prices in recent months. The Chilean National Copper Company said that copper production in January-June was 798,000 tons, down from 843,000 tons in the same period last year. During this period, the company's profit before tax was US$1.023 billion, and the loss in the first half of 2016 was US$97 million. Cash costs increased from $1.275 per pound in 2016 to $1.317, as the ore grade of the company's mines declined.

In September, Chappy Hakim, former chief executive of Freeport McMoRan Inc., said that although the company had reached a milestone agreement with the Indonesian government, Freeport still faces the control of the copper mine. huge challenge. Freeport said it will transfer 51% of the Grasberg copper mine and establish a second smelter in Papua, while also committing to invest about $20 billion in the Grasberg mine. Correspondingly, Freeport can “immediately†apply for a three-year extension of the mining license from 2021, and is expected to be extended to 2041, during which the Freeport will have to pay a higher tax burden. But the biggest problem at the moment is how much the shares are valued and who will buy them.

In September, Southern Copper CEO Oscar Gonzalez said the company is considering bidding for the Michiganlay copper development rights as it expects copper prices to rise further in 2019. He also said that the company will begin environmental impact assessment of the LosChancas copper mine in Peru early next year. He said that copper prices are expected to be between 2.60 and 2.90 US dollars per pound in 2018. Since 2019, copper prices may rise further.

According to the overall situation, the supply prospects of the top ten copper concentrate enterprises in the fourth quarter are not much changed. The current capacity flexibility space is not large, and the newly added mines will not be able to form capacity in the short term.

|

Strike threats in major mines:

An important risk of copper supply in 2017 is the risk of strikes brought about by wage negotiations, after the strike risk has been reflected once.

In August, an executive at BHP Billiton said that its Chilean Escondida copper mine recovered faster than expected after six weeks of strikes, and production is now at normal levels. Escondida is the world's largest copper mine, and the strike of the mine has had an impact on the copper market in February and March. The union representing the striker chose to resume work under the old contract, thus delaying negotiations on the new contract until next year. Danny Malchuk, president of BHP Minerals Americas operations, said that employers and employees may return to the negotiating table early. "There is a special team to solve this problem, we do not rule out this possibility." "If this possibility is realized, I think it will be at the end of this year or the first quarter of next year."

Overall, the Escondida copper mine is currently only BHP Billiton to pay the bonus to quell the risk of a short-term strike again, but the core salary issue is still not achieved, so the risk of strikes still exists.

However, the strike at the Escondida copper mine did not give workers much benefit, which would cause other mine union strikes to be somewhat inhibited.

In May, the Chilean Collahuasi copper miners and the employers issued a joint statement saying that the two sides have reached a new agreement, which is valid until 2020. According to the agreement, 1,485 union workers in the Collahuasi copper mine will not raise wages, but each person will receive a one-time bonus of 11 million pesos (about 16,400 US dollars), and also get 3 million pesos without interest. loan. 70% of union workers voted for the latest agreement. Jorge Gomez, president of the Collahuasi Copper Mine, said in a statement that the agreement focuses on safety, productivity and sustainability, reflecting the willingness of both parties to achieve a win-win situation. The latest agreement will take effect at the end of October when the existing contract expires, valid for three years, or may help reduce the risk of long-term strikes in Chile's large copper mines in the next few years.

In June, Codelco and its El Teniente mine union signed an agreement to guarantee the number of workers with minimal service in case the next round of salary negotiations led to a strike. Under the new labor rules, these agreements are encouraged and considered a good sign before collective bargaining.

In July, two copper mines under Antofagasta Plc faced a strike threat, in which the Zaldivar copper mine entered a strike. However, Antofagasta has reached a new salary agreement with the head of its Centinela copper mine to lift the mine's strike risk.

In August, a representative of the Office of the Ombudsman said on Friday that Peruvian protesters had cleared a roadblock on a road used by Minmetals Resources (MMG Ltd), after the government had declared a state of emergency. Through this road, the company transports the copper concentrate produced by the Las Bambas copper mine to the port. Peruvian President Pedro Pablo Kuczynski announced on Wednesday that the region was in a state of emergency, which suspended the right to assembly and other constitutional rights. Minmetals Resources said, however, that the production of the Las Bambas copper mine has continued during the road blockade.

In general, since the mine is still strict with cost control, it mainly does not increase the fixed salary, but increases the one-time bonus. From the above-mentioned several agreements, basically one-off bonuses are mainly used. The overall supply risk has not been completely eliminated. In addition, there are potential conflicts between Peruvian mines and local communities. However, the Peruvian government is committed to mining development and will not pose too much risk in the short term.

On the whole, the main risk of copper mine strikes brought about by salary negotiations in 2017 has been released, so the supply risk brought by salary negotiations has been small. The supply risk in the fourth quarter is mainly due to the negotiation of processing fees.

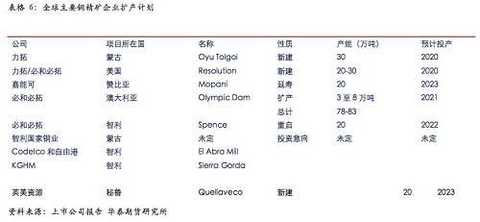

Ten major copper concentrate enterprises expansion:

The long-term expansion of the top ten copper concentrate enterprises is mainly based on Rio Tinto and BHP Billiton. Both of these companies are very optimistic about the long-term prospects of copper; the mines are relatively large, but they will basically be put into production after 2020. In the latest situation, both BHP Billiton and Chile's national copper industry have expanded their mineral activities.

In addition, Glencore Africa's mines are mainly based on reducing costs and extending life, by introducing new mines and introducing new equipment. Earlier, Glencore said that the African mine will resume production in 2018. According to the current movement, the resumption of Glencore can still be maintained in 2018. In addition, Glencore can strengthen the acquisition and layout of mines in Africa, that is, the impact on the supply of copper in Africa is increasing, and the concentration of copper supply in the world may be further enhanced, which is more favorable for copper prices, especially in anticipation of lack of increase. The amount of the case.

Overall, from 2017 to 2020, the top ten copper concentrates are currently only in 2018. Glencore can increase copper supply due to the resumption of production in Africa. However, as the total amount is only 200,000 tons, and other miners have no production increase projects, and capital expenditures are limited under the efforts of still reducing costs, the overall outlook for the output of the top ten copper concentrate enterprises is declining.

However, from the situation in recent months, Anglo American and Glencore are also working hard to strengthen the expansion of copper resources, playing a more active role in the new round of copper mine expansion in Peru; plus BHP Billiton, force Tuo, Chile's national copper industry, as a whole, most of the international top ten copper concentrate enterprises are driven by the prospect of copper price, and have acted.

|

In September, Anglo American's Peruvian head Luis Marchese said that before the company's implementation of the Quellaveco copper project in Peru, the company will start the formal process of selling a majority stake in the project. The company's implementation of the Peruvian copper project is expected to begin in mid-2018.

Other enterprise expansion plans:

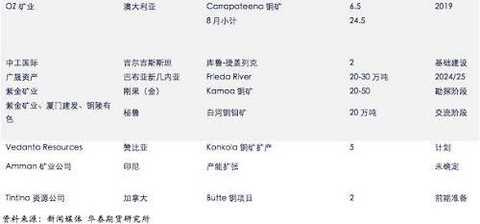

In addition to the top ten copper concentrate enterprises, in the first half of 2017, there were not many new copper mine expansion projects, mainly because the previously invested mines began to gradually form capacity.

In April, Zijin Mining (601899, shares) reported that the Kolwezi copper mine project in Congo (King), the project is intensifying construction, is scheduled to start production in 2017, the planned production capacity is 5.8 per year. Ten thousand tons. In addition, there is currently no construction schedule for the Kamoa copper project. In June, the Zijin Mining Congo project has begun to mine.

In addition, Tongling Nonferrous (000630, shares it) Mirador copper mine short-term actual output is only about 100,000 tons, and or a stable supply from 2018.

In July, the leaders of Tongling Group inspected the Mirador copper mine, and others did not track the increase in mines.

In August, Canada informed Tintina Resources that it was approved for the Butte copper project; so far, Tintina has spent $50 million to $60 million to develop mines. In the coming year, it plans to spend another 5 million to 6 million US dollars. Shanahan said the new mine is expected to cost $250 million.

From the situation of tracking in the third quarter, other companies have less expansion plans. The new plans are mainly based on Peru and Chile, and traditional large enterprises have advantages. The total increase of other mines in other mines in 2017 is about 208,000 tons. In 2018, other mining companies are expected to increase by 285,000 tons; in 2019, it is expected to increase production by 245,000 tons.

|

|

In general, in 2017, 2018, and 2019, the supply of new copper mines is not much. Therefore, the total supply of refined copper actually depends on the supply of copper concentrates. In addition, due to the low supply growth rate, If global copper demand maintains moderate growth, the tight supply of refined copper will remain.

In addition, in the previous July and August, we tracked the ambitious development plans of Peru and Chile. The total planned capacity is relatively large. However, the future copper project in Peru is mainly in the hands of the government, but has not yet been implemented into specific enterprises. This is The plan announced by the government is huge, but the plan seen from the perspective of corporate statistics is much smaller. We believe that the capacity building in Chile and Peru can only be realized if it is specifically implemented in the enterprise.

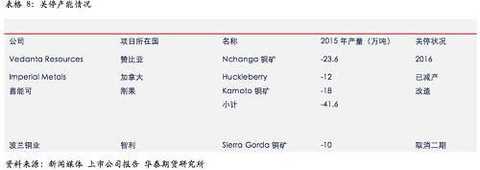

Previously stopped production of mines:

In addition to the top ten copper concentrate enterprises, there was no news of a large company's production cuts in the first quarter. Due to the upward price of copper, the current closure of mines needs to consider the possibility of their resumption of production. In 2016, the shutdown production outside the top ten copper concentrates is currently around 240,000 tons.

In May, Polish copper canceled the restart of the second phase project of the Sierra Gorda copper mine in Chile; mainly due to the high investment cost of the Sierra Gorda copper mine in Chile, and the current copper price is not enough to stimulate the continued investment of the Polish copper industry.

However, in August, from the information released by the Chilean government, Polish copper investment in the Sierra Gorda copper mine will continue.

|

Global mine structure change trends:

Since 2017, mergers and acquisitions between mines have been active;

|

In March, Anil, president of Vedanta Resources, the largest copper producer in London. Anil Agarwal made a bold move to acquire up to 12% of Anglo American's shares. The London-listed mining company Anglo American has been the main competitor of Vedanta Resources, which he runs.

In addition, Vedanta Resources said it will invest $1 billion in its Konkola copper project in Zambia to create 7,000 jobs. This means that Vedanta Resources, the Konkola copper mine has increased again based on current production, and with the Nchanga copper mine, Vedanta Resources itself has nearly 200,000 tons of minerals in Zambia. If you join forces with Anglo American, a global copper mine group with more than one million tons will be re-emerged globally, which increases the risk of further concentration of global copper resources.

In April, Antofagasta CEO Ivan Arriagada said that in the case of limited investment, mining companies will focus on investing in existing businesses to improve degraded ore quality and boost production. When asked if Antofagasta would consider buying Rio Tinto's stake in the Grasberg mine in Indonesia, Arriagada said, “Like other opportunities, as long as we enter the market, we will consider it.†Hennie, Head of Copper, Anglo American Faul said that it is feared that Antofagasta will still be difficult to convince the board and shareholders to invest heavily.

In May, BHP Billiton said that the company has started plans to sell the Cerro Colorado copper mine in Chile, which is currently in the early stages of evaluation, and the final decision has not yet been made, and it is still unclear whether a sale agreement will be reached. The Cerro Colorado copper mine is located in the Tarapacá region of Chile and produced 77,000 tons of copper in FY2016.

In June, China Polymetallic announced that the company's subsidiary Huaxing Global and Ruilinadi Co., Ltd. entered into the agreement, pursuant to which Huaxing Global has the condition to agree to acquire the mining rights of the Myanmar copper-lead mine for a total consideration of RMB 49 million. According to the announcement, the mining right can cover about 49.59 acres of copper lead in the No. 2 mining area of ​​Hongtukengshan, Banshan Village, Twilight Town, Mandalay Province, Myanmar, from December 24, 2014 to December 23, 2019. The mine conducts mining and development of minerals. The copper and lead reserves of the Myanmar mines are classified into 331, 332 and 333, with an estimated resource of 1,284,500 tons.

In June, a senior official at Volcan, the largest zinc and silver miner in Peru, said the company was looking for mergers and acquisitions in copper projects to diversify the company. The executives are evaluating potential M&A opportunities with a focus on the Chumpe and Carhuacayán copper mines in the north of the country, as well as the Rica Cerrea copper mine.

In August, EMR Capital said it would buy an 80% stake in the Lubambe copper mine in Zambia from ARM (African Rainbow Minerals) and its partner Vale International; the company bought a stake in GoldenGrove copper-zinc mine from MMG in December last year. “EMR will continue to focus on industries such as copper, gold and coking coal through global mergers and acquisitions.â€

On September 20th, Anil Agarwal, president of Indian billionaire and diversified minerals company Vedanta, said his family-held trust fund has increased its stake in Anglo American but is not prepared to win the entire Anglo American group. stock. In a statement, Anil Agarwal said that in March, it spent $3.25 billion to increase its holding of 12.43% of Anglo American, which means that the total number of shares held by Anglo American will increase to 20% in the next 10 days. . Obviously, Vedanta's behavior is consistent with the purchase of Zambian mines in March. From its increase in shares of Anglo American, its right to speak in the global copper market has further increased.

In September, Canadian miner First Quantum Minerals said it had increased its stake in Minera Panama to 90% to increase copper output. The increase in the company’s shares caused it to pay a cost of 635 million yuan. Previously, the company held an 80% stake in Minera Panama, which was transferred from Korean miner LS-Nikko Copper.

Judging from the M&A transactions tracked in 2017, it is mainly based on companies other than the top ten mining companies. Through equity mergers and acquisitions, copper resources can be quickly obtained, but because it is only the conversion of existing capacity, therefore, The new capacity is not very helpful.

Global copper concentrate cost curve changes:

The average cost of copper mines in the world's major miners has not changed much. For copper prices, it has been difficult to rely on miners to reduce costs to bring profits, and the decline in copper grades is a common problem over time. The cost change for the overall native refined copper is uplifting.

In addition, from the structure of cost reduction in 2016, the mine decline method is not uniform, but there is no means to reduce investment and increase in by-product income, but these are not sustainable and are easy to rebound.

|

In addition, according to the report of the Chilean Mining Association, the current cash cost of domestic copper concentrates in Chile is generally higher than other copper producing areas (except Africa and other places); due to the new production capacity of copper concentrates we track, the 2017 increase is almost Very small, so the supply and supply guarantee in production is very important, and Chile's national copper is a benchmark.

From our previous calculations, the national copper industry in Chile is only slightly cautious to survive below US$5,000/ton; if the ground mining is transferred underground, the price of copper required will be more than US$5,500/ton. Therefore, the margin of safety for late copper prices may be between $5,000 and $5,500/ton. However, since the price of copper in the third quarter has entered the range of 6,000-7,000 US dollars / ton, the cost is not significant.

Global copper mine exploration activity tracking:

From the situation tracked in 2017, copper mine exploration activities are also becoming increasingly active.

|

In August, Sol Gold announced that drilling in the Cascavel copper-gold mine in Ecuador has become one of the most important achievements in the history of copper and gold exploration in the world. According to the 0.1% copper equivalent grade, the 23R hole of the Alpala deposit is 1030 meters deep at 490 meters, the copper grade is 0.59%, and the gold grade is 0.9 g/ton, ie the copper equivalent is 1.16%. According to the 1.5% cut-off grade, the thickness of the ore is 216 meters from the depth of 970 meters, the copper grade is 1.29%, the gold grade is 2.84 g/ton, or the copper equivalent grade is 3.08%. According to the company, the borehole is estimated to be the world's top 20 copper and gold mine drilling results, with a total copper equivalent grade of 1.195%. The amount of resources is expected to be announced for the first time

In July, Phoenix Mining hopes to meet the growing demand for copper by restoring the Empire mine discovered in the 1880s but discontinued in 1942. Phoenix Mining CEO Dennis Thomas said that now is the "perfect time" to develop a new copper mine, and the production of the Empire mine is expected to open in 2020. Phoenix Mining hopes to use the historical data of the Empire mine to determine the reserves of the mine based on 287 mines drilled by the former owner. Thomas said he expects the mine's shallow areas to produce gold, silver and tungsten, most of which remain to be developed.

In June news, Wanbao Minerals and Havilah signed a memorandum of cooperation to promote the completion of the pre-feasibility study for the KalKaroo project. Previously, Wanbao Mining conducted a six-month due diligence on the project. Recently, Havilah also announced the upgrade of KalKaroo resources. The results of the pre-feasibility study will provide a basis for the resolution of whether Marlboro Minerals participates in the financing and development of the KalKaroo project.

In addition, in June news, the First Institute of Geology and Mineral Exploration of the Shandong Bureau of Geology and Mineral Resources recently discovered a large copper deposit in the town of Wapsa, Soluxunbu County, Nepal, with an average grade of 7.9%. The amount of resources has reached a large scale. It is understood that this is the first large copper mine discovered in Nepal, and its high quality is rare in the world.

In May, KGL Resources acquired the land lease rights for a potential copper resource in the Jervois region of central Australia. Wood said that there are good indications that the copper mine is extending north from the Jervois area to the lease of the Unca Creek area.

In April, Canada's Inomin Mining recently announced that the company's first gold-copper-zinc complex exploration project at King's Point has been submitted to the Newfoundland and Labrador Natural Resources Department. The company plans to focus on the newly confirmed deposits in the past two years, focusing on the Rendall-Jackson copper-gold VMS deposit that has been mined in the area. The company expects that in mid-May, after receiving the exploration license, exploration work including the use of polarization/resistivity and high-resolution magnetometers in the priority areas will be gradually implemented.

Carube Copper Corp. (CUC.V) President and CEO Jeff Ackert confirmed that Carube Copper has received a formal transfer document from the Jamaica Ministry of Transport and Mines and will have a special exploration and exploration license previously held by OZ Minerals. Carube Copper currently owns all of the 11 exploration licenses covering 535 square kilometers of Jamaica.

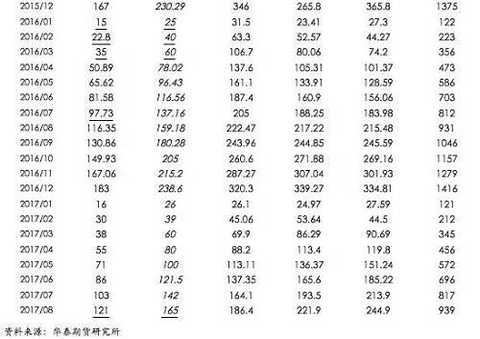

Country data to see the global supply of copper concentrate:

|

From the perspective of the country,

In September, the Peruvian Ministry of Mines and Energy said that in the first seven months of this year, Peru's copper, zinc and iron production increased, and gold and lead production declined. Copper production in January-July was 1.38 million tons, an increase of 4.3% over the same period last year. The effect of the previous round of capacity production has gradually decreased, and according to the previous Peruvian official estimate, Peru's copper production in 2018 is still flat.

In September, Chilean central bank statistics showed that in August, the export volume of Chile's mineral products hit a new high since December 2014. The export value of mineral products in August was 3.30 billion US dollars, compared with 2.46 billion US dollars in the same period last year. The increase was 34.5%, and the chain increased by 22.4%. In the first eight months, Chile’s exports of mineral products totaled US$21.9 billion, an increase of 13.5% from US$19.3 billion in the same period last year. In August, Chile’s copper exports amounted to US$2.99 ​​billion, an increase of 33.7% from US$2.24 billion in the same period last year, and a year-on-year increase of 22.2%. Among them, the export value of electrolytic copper was 1.421 billion US dollars, and the export volume of concentrate copper was 1.396 billion US dollars.

At the end of July, the Chilean National Copper Council (Cochilco) said that the average global copper price in 2017 is expected to be $2.64 per pound, slightly higher than the previous estimate of $2.60 per pound, mainly due to increased demand in China. The Chilean National Copper Council also expects Chile's copper production in 2017 to be about 5.6 million tons, an increase of 0.8% from the previous year, roughly in line with the previous April valuation. The committee expects Chile's copper production to increase to 5.9 million tons in 2018. Chilean mining minister Aurora Williams said that part of the increase in copper prices in 2017 was due to better performance of China's economic indicators, exceeding market expectations. At present, China is an important export market for Chilean copper. China's economy has improved, especially in the field of copper consumption, such as real estate, which will benefit the Chilean copper market.

In April, the Chilean National Copper Council (Cochilco) estimated that the country's 2017 copper output is expected to be slightly less than 5.6 million tons, previously estimated at 5.79 million tons, adjusted production estimates mainly due to BHP Billiton's Escondida copper mine strike influences. In its quarterly report, the committee said that the Escondida copper mine was shut down for 43 days in the first quarter, forcing it to repair 180,000 tons in January. The latest estimate is 0.8% higher than the 2016 production. Commission Executive Vice-President Sergio Hernandez said in a statement that the year-on-year increase in production was partly attributable to the lower 2016 data, which fell by 3.8% in Chile.

In terms of Africa's supply, Congo and Zambia still have potential to increase. This year and next year, the increase is mainly driven by prices. In 2018, it will increase the number of new years, mainly the resumption of Glencore and the expansion of some mines.

In September, the Zambian Ministry of Mines said that Zambia's copper production this year is expected to decline slightly to 753,992 tons, down from 774,290 tons in 2016, mainly due to the decrease in production of the Konkola copper mine. Paul Chanda, the managing secretary of the Zambian mining ministry, said the Konkola copper mine is expected to reduce production by 40% this year. Lumwana copper production is expected to decrease by 15%.

But then, a report released by the Zambia Chamber of Mines said that it is conservatively estimated that Zambian copper production is expected to increase to 800,000 tons by the end of this year. Between 2000 and 2014, the country attracted $12.4 billion in mining investment, and currently six mining companies in the country are operating. The country will recapture the throne of the largest copper producer in the African region. “This is only a conservative production estimate, and the Zambian government’s production estimate is close to 850,000 tons.â€

In addition, the Mirador copper mine in Ecuador actually reached or continued until 2018. Since the current equipment capacity is limited to 100,000 tons, it is estimated that it will not increase in 2017, mainly in 2018.

Therefore, based on the situation in August, from the perspective of country, Chile and Peru and Indonesia's copper supply elasticity in 2017 is not particularly large compared to 2016, of which Chile's supply elasticity or relative increase of 2016 is only 30,000. Tons, while Peru’s latest production forecast, our elasticity increase is about 100,000 tons, Congo and Zambia supply elasticity is 50,000 tons respectively, and Indonesia’s free port is re-exported, Indonesia’s incremental elasticity is maintained at 150,000. Tons, the overall 2017 copper mine has an incremental elasticity of 410,000 tons.

In 2018 and 2019, Chile, Peru, Zambia, Congo, etc., the overall new capacity added is relatively small, and the increase in output elasticity is expected to be relatively small. In addition, the supply elasticity of copper mines in 2018 is mainly based on Chile and Africa, mainly due to the resumption of production of the mines that were previously disturbed or shut down. The recovery flexibility of Chilean mines has been seen in 2017, so the impact on 2018 is somewhat reduce.

Looking at the long-term investment potential from the country:

In terms of investment, the actual investment potential of both Chile and Peru has not been fully explored, mainly interrupted by low copper prices.

From the perspective of Chile, from May 2017, there have been some changes:

Mainly Poland's copper industry canceled the second phase of the Sierra Gorda copper mine in Chile, which is mainly related to the overall higher investment cost of Chile's copper mine. The current copper price still does not support the new investment of Chilean copper mine.

In addition, Chile's biased labor system also makes copper investment a certain risk, and Chile's investment costs are generally high, so the current market conditions are not enough to support a new round of large-scale development of Chile's copper mine.

However, the August situation shows that the rise in copper prices and prospects have already touched Chile’s desire to invest:

In August, the Chilean government said that mining companies are planning to invest about $65 billion in Chile over the next decade, an increase of about a third from previous estimates. Chilean mining minister Aurora Williams said that more than 90% of them are copper projects. Larger projects include the resumption of the El Abra Mill mine and the Sierra Gorda 2030 ktpd mine, the former being a joint venture between the Chilean state-owned copper company Codelco and the Freeport McMullen Copper Company, which is controlled by the Polish miner KGHM. .

If converted according to 90% of the investment, the approximate investment amount is about 58.5 billion US dollars. According to Chile's investment cost of about 200 million US dollars / ton of copper, the potential incremental capacity is about 2.93 million tons, which is further increased than previously expected.

And the Peruvian investment:

In May 2017, Peru’s Minister of Energy and Mines Gonzalo Tamayo announced that three large copper projects will be launched in 2018, namely Quellaveco, Justa and Michiquillay, with a total investment of $7.272 billion. The Minister also stressed that Peru's mining projects currently account for 6% of the world's total, ranking first in Latin America.

In July 2017, following the project announced in May, Peruvian officials said they expected copper production to make a huge breakthrough in the next few years. The data comes from the Center for Competitiveness and Development of San Martin de Porres University in Peru and the Institute of Mining Engineers of Peru. According to the two organizations, 18 copper projects will be put into production by 2021.

|

This means that as long as the price of copper is right, only Chile and Peru, the potential investment capacity can reach 6.5 million tons.

However, from the tracking situation in September, it is not easy to implement these potential investment capacity.

Lima September 19 news, Peru's Minister of Energy and Mining Cayetana Aljovin said that by 2021 Peru's copper production will exceed 3 million tons. Peru’s copper production last year was 2.35 million tons, and Peru is the second largest copper producer in the world. Aljovin said the government is committed to increasing investment in mining exploration. This means that before 2021, the conversion of copper mines in Peru increased to about 650,000 tons, and these production capacity is roughly equal to the plan announced by the Peruvian government in May, while other project plans have not yet been reliably implemented.

In September, Chilean mining minister Aurora Williams said that Chile's copper production accounted for more than a quarter of global production last year. If the investment project goes well, Chile may increase production by 20% in the next 10 years. In an interview, Williams said that by 2028, copper production could rise from 5.5 million tons last year to 6.6 million metric tons. This year's mine investment has increased by 32% to reach $65 billion, which is a good sign for the Chilean mining industry. The rise in copper prices has spurred the world's largest copper producer to start looking for more minerals. This means that the actual capacity conversion of Chile's mines is also more difficult. In the next decade, Chile's supply expansion plan is only 1.1 million tons.

Therefore, judging from the tracking situation in September, the actual new mines in the future will not be as intense as planned. If the price does not improve excessively, the future supply will grow at a lower rate on average; this will eliminate the supply side of copper prices. Risk, the future copper price is essentially dependent on whether there is any surprise in the demand. As long as the demand is not too bad, the price of copper is generally bullish.

In addition, from the information in September, the release of Chile in the next 10 years is relatively mild, while the increase in Peru before 2021 is relatively mild, and the investment in 2022-2028 is not certain; during this period, globally, copper The increase that demand can see is mainly electric vehicles, infrastructure improvement in developed countries, infrastructure development in developing countries, and transformation of China's distribution network. Therefore, there is a possibility of unexpected surprises in demand. Therefore, in the big direction, copper prices are not available. Turn.

Long-term copper mine & smelting capacity:

In China, the situation tracked in August showed that there was no further new refining capacity plan. The new refining capacity plan in the first quarter was mainly in the Minmetals project in February.

In July, the situation was mainly due to the gradual trial production of some refined copper projects. Therefore, the refining capacity in 2017 mainly depends on the production capacity of the previously planned production capacity. At present, in terms of various situations, the maximum increment of China's refining capacity in 2017 may not exceed 750,000 tons. It is estimated that China's actual refining capacity will be added in 2017. Near 450,000 tons. However, due to the increasingly small elasticity of copper concentrates, if the refining capacity is put into 2017, it will inevitably lead to a further decline in copper concentrate processing fees. Estimated from the situation in July, the elasticity of copper concentrate supply is around 420,000 tons, and the previous copper mine elasticity estimate was maintained in August.

|

In foreign countries, new smelting capacity was not tracked in the third quarter.

|

In terms of overall situation, in terms of future new capacity in the world, there are still 450,000 tons of new capacity waiting for launch in the fourth quarter of China, but after the completion of the launch, the smelting capacity will come to an end. The more long-term outlook is that the two projects of Yunnan Copper in Inner Mongolia and Fujian, as well as the projects of Minmetals, will be put into effect in about 2019. So far, China's new smelting capacity will come to an end.

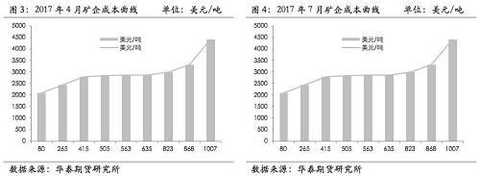

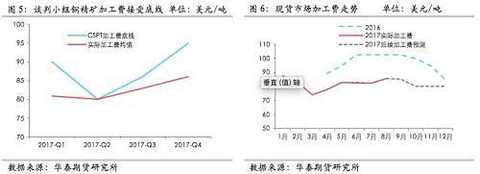

Copper concentrate processing fee:

In July, the China Copper Raw Materials Joint Negotiation Group (CSPT) set a third-quarter processing fee bottom line of $86/ton and 8.6 cents/lb; this is higher than the second-quarter processing fee procurement bottom line, however, due to the second quarter processing fee In fact, it is a high process, so the processing fee bottom line in the second quarter has not been touched.

However, the bottom line of processing fees in the third quarter is relatively high, which is almost the high range of current spot processing fees. Therefore, the bottom line of processing fees in the third quarter actually has a certain inhibitory effect on the procurement of refined copper enterprises.

In August, the overall processing fee maintained a steady decline, and the processing fee in the spot market was already lower than the bottom line set by the negotiating team. Therefore, it has a strong inhibitory effect on the procurement of processing fees for smelting enterprises.

From the perspective of copper concentrate imports in the third quarter, the bottom line of processing fees has a strong limiting effect on procurement.

In September, the China Copper Raw Materials Joint Negotiation Group (CSPT) set a bottom line for processing costs in the fourth quarter of $95/ton and 9.5 cents/lb; in order to win the bargaining for future annual long-term negotiations. Once the processing fee is set, this will have a greater constraint on member companies. Unless the spot processing fee is higher than the bottom line, it will still greatly limit purchases.

å› æ¤ï¼Œå››å£åº¦ä¸»è¦å…³æ³¨çŽ°è´§åŠ 工费对于国内精炼铜供应的影å“,我们认为会é™åˆ¶ç²¾ç‚¼é“œäº§é‡ã€‚

|

å›½å†…å†¶ç‚¼äº§èƒ½å¢žåŠ ï¼Œå†¶ç‚¼è‡ªç»™èƒ½åŠ›å¢žåŠ ï¼š

综åˆæƒ…况æ¥çœ‹ï¼Œéšç€2016-2017年精炼产能之åŽï¼ŒéšåŽçš„原生铜冶炼项目开始å‡å°‘,虽然远期投产计划ä¸ä¾ç„¶æœ‰å—国铜二期20万å¨ã€èµ¤å³°äº‘铜二期30万å¨ã€é»‘龙江紫金10-15万å¨ç¾çº¦å’Œä¸é“东å—铜业40万å¨ç¾çº¦é¡¹ç›®ï¼Œä½†æ˜¯å› ä¸ºæ— æ˜Žæ˜¾æ—¶é—´è¡¨ï¼Œå› æ¤é›†ä¸æŠ•æ”¾çš„æ¦‚çŽ‡è¾ƒä½Žï¼Œå› æ¤åŽŸç”Ÿé“œå†¶ç‚¼é¡¹ç›®æ–°å¢žå¹…度是放缓的。这也和全çƒé“œç²¾çŸ¿ä¾›åº”的增速趋势较为一致。æ¤å¤–,å‘改委å‘布的å三五规划已ç»æ„识到精炼产能投放的问题,已ç»å¼€å§‹æ”¿ç–性约æŸï¼Œä¸Šè¿°è®¡åˆ’产能或已ç»æ˜¯ä¸å›½ç²¾ç‚¼é“œäº§èƒ½çš„高峰。

å››å£åº¦ï¼Œæ½œåœ¨æœ‰45万å¨äº§èƒ½æŠ•æ”¾ï¼Œå¦‚果这些产能集ä¸æŠ•æ”¾ï¼Œæˆ–使得整体产能利用率下é™ã€‚

|

è¿™æ„味ç€å†ç”Ÿé“œè®¡åˆ’产能已ç»é«˜è¾¾80万å¨ï¼Œæ‰€ä»¥ï¼Œä»Žé•¿æœŸä¾›åº”的角度æ¥çœ‹ï¼Œé“œä¾›åº”虽然从原生铜的压力下逃脱,但是å†ç”Ÿé“œä¾›åº”的压力é€æ¥æ˜¾çŽ°ã€‚ä¸è¿‡åºŸæ—§é“œä¾›åº”å¤ªè¿‡ç´§å¼ ï¼Œä»Žå三五规划æ¥çœ‹ï¼Œå†ç”Ÿé“œå 比增é‡ä»…å¢žåŠ 2%,当å‰ç²¾ç‚¼é“œä¾›åº”的主è¦åŠ›é‡ä»ç„¶æ˜¯åŽŸç”Ÿå†¶ç‚¼äº§èƒ½ã€‚

精炼铜需求:

从数æ®æ¥çœ‹ï¼Œ2017å¹´1-7月份,全çƒé“œè¡¨è§‚需求基本上是以负增长为主,ä¸è¿‡ï¼Œ7月份全çƒé“œè¡¨è§‚需求åŒæ¯”出现较大增幅;主è¦æ˜¯å…¨çƒè´¸æ˜“活动é€æ¥å›žå‡ã€‚

|

除去ä¸å›½ä¹‹å¤–,欧洲ã€ç¾Žå›½ã€æ—¥æœ¬é“œè¡¨è§‚需求表现ä¸ä¸€ï¼Œæ¬§æ´²ã€ç¾Žå›½åŒæ¯”æ•°æ®æ¯”较好,但环比å˜åŒ–ä¸æ˜¯å¾ˆæ˜Žæ˜¾ï¼Œæ—¥æœ¬é“œéœ€æ±‚整体有一定增长。

|

从铜需求展望æ¥çœ‹ï¼Œæ¬§æ´²ã€ç¾Žå›½ã€æ—¥æœ¬é“œéœ€æ±‚点主è¦æ˜¯ä»¥ç¾Žå›½ä¸ºä¸»ã€‚

æ¤å‰æˆ‘们已ç»å¯¹å·æ™®çš„扩大基础设施建设对铜需求进行了分æžï¼Œå¦‚下:

2017å¹´ç¾Žå›½é“œéœ€æ±‚æ˜¯æ— æ³•å—到实际的刺激,而由于目å‰æ¥çœ‹ï¼ŒæŠ•èµ„总é‡ä»ç„¶åœ¨1万美元左å³ï¼Œå› æ¤ï¼Œæ€»éœ€æ±‚å‰çž»ä¾ç„¶ç»´æŒæ¤å‰æˆ‘们的折算。

ç»´æŒå¯¹ç¾Žå›½åŸºå»ºéœ€æ±‚的测算,如下:

对于é“è·¯ã€æœºåœºã€æ¡¥æ¢ï¼Œä¸å›½çš„æ•°æ®æˆ–比较有对比性,并且,ä¸å›½çš„投资还主è¦æ˜¯ä»¥è½¨é“交通和é“路为主,对铜的需求è¦æ›´å¼ºä¸€äº›ã€‚å› æ¤ï¼Œç¾Žå›½é“è·¯ã€æœºåœºã€æ¡¥æ¢å¤§è§„模建设对铜的需求总é‡æ¯å¹´çš„增é‡å¯èƒ½åœ¨15万å¨/年以内(如果扣除é“电缆的份é¢ï¼Œé“œéœ€æ±‚就低于10万å¨/年了)。

而å·æ™®å›½ä¼šæ¼”讲并未æç”µç½‘æ”¹é€ ï¼Œè¿™æˆ–æ„味ç€ç”µç½‘æ”¹é€ å¹¶éžå…¶ä¼˜å…ˆéƒ¨åˆ†ï¼Œæˆ–者是其所å 份é¢è¾ƒä½Žï¼Œè¿™å¯¹äºŽç¾Žå›½é“œéœ€æ±‚预期实际上都ä¸åˆ©ï¼Œä¸è¿‡ï¼Œæˆ‘们估算的增é‡ä¹Ÿæœ€å¤§ä¹Ÿåªæ˜¯15万å¨/å¹´ï¼Œå› æ¤ï¼Œå®žè´¨å½±å“并ä¸æ˜¯ç‰¹åˆ«å¤§ã€‚

而电网建设领域,

美国电网迄今已有100多年的建设å‘展历å²ï¼Œæœ€åˆæ˜¯ç”±ç§è¥å’Œå…¬è¥ç”µåŠ›å…¬å¸æ ¹æ®å„自的负è·å’Œç”µæºåˆ†å¸ƒç»„æˆä¸€ä¸ªä¸ªå¤ç«‹çš„电网,éšåŽåœ¨äº’利原则基础上通过åŒè¾¹æˆ–多边åè®®ã€è”åˆç»è¥ç‰æ–¹å¼ç›¸äº’è”网,é€æ¥å½¢æˆäº†ä¸œéƒ¨ã€è¥¿éƒ¨å’Œå¾·å…‹è¨æ–¯ä¸‰å¤§è”åˆç”µç½‘,这三大è”åˆç”µç½‘之间仅由少数低容é‡çš„ç›´æµçº¿è·¯è¿žæŽ¥ï¼Œåˆ†åˆ«å 美国售电é‡çš„73%ã€19%å’Œ8%。

美国的输电网纵横交错,常è§çš„电压ç‰çº§æœ‰765åƒä¼ã€500åƒä¼ã€345åƒä¼ã€230åƒä¼ã€161åƒä¼ã€138åƒä¼ã€115åƒä¼ã€‚æ®ç¾Žå›½èƒ½æºä¿¡æ¯ç½²ï¼ˆEIA)统计,2012年美国200åƒä¼ä»¥ä¸Šé«˜åŽ‹è¾“电线路有30.7万公里,其ä¸åŒ…括约3888公里的765åƒä¼äº¤æµè¾“电线路,以åŠ3545公里±500åƒä¼ç›´æµè¾“电线路。

美国输电网投资自上世纪70年代以æ¥ä¸€ç›´è£¹è¶³ä¸å‰ï¼Œè€Œä¸”长期滞åŽäºŽç”µåŠ›éœ€æ±‚å’Œå‘电容é‡çš„增长。由于输电投资水平低,跨州ã€è·¨åŒºç”µç½‘è”系薄弱,输电能力ä¸è¶³ï¼Œé€ æˆäº†è¾“ç”µç“¶é¢ˆï¼Œä½¿æ‹¥æœ‰å»‰ä»·ç”µçš„å·žæ— æ³•é€è‡³ç”µåŠ›ç¼ºä¹çš„州,所以美国亟须建设新的输电线路。美国输电网投资ä¸è¶³çš„åŽŸå› åŒ…æ‹¬ä¸¤æ–¹é¢ï¼Œä¸€æ˜¯è·¨å·žè¾“电项目建设需è¦å¤šä¸ªå·žçš„监管部门åŒæ„,有时还è¦å¤šä¸ªè”邦政府部门åŒæ„,审批程åºå¤æ‚ã€å®¡æ‰¹æ—¶é—´é•¿ã€èŽ·å¾—批准难;二是输电项目投资回报低ã€å»ºè®¾å‘¨æœŸé•¿ï¼Œä¸Žå…¶ä»–领域相比缺ä¹æŠ•èµ„å¸å¼•åŠ›ï¼Œå½±å“了输电项目建设资金的ç¹é›†ã€‚

从一些基础资料æ¥çœ‹ï¼Œç¾Žå›½ç”µç½‘当å‰æœ€äºŸå¾…建设的是输电网,特别是跨区域的输电网建设。而输电网建设对铜的需求比较薄弱,铜需求主è¦é›†ä¸åœ¨é…电网领域。

å¦å¤–,美国é…电网有其独特的历å²ï¼›é“和铜在低压电网领域的应用之争由æ¥å·²ä¹…,æ®åŸºç¡€èµ„料显示,早在60年代,ä¸ç¾Žå‡å·²ç»è®¤è¯†åˆ°é“œèµ„æºçš„稀缺性,å‡ç€æ‰‹ç ”制é“电缆。ä¸è¿‡ï¼Œä¸å›½é“电缆åˆæœŸå› æŠ€æœ¯åŸºç¡€è–„å¼±ï¼ŒåŠ ä¸ŠéšåŽä»Žæ‹‰ç¾ŽèŽ·å¾—了铜资æºï¼Œå› æ¤é“œç”µç¼†å°±æˆä¸ºä¸»å¯¼ã€‚而美国,80年代末,é“电缆开始æˆç†Ÿï¼Œå› æ¤åŒ—美市场é“电缆和铜电缆å„å æ®50%(目å‰å…¨ä¸–界范围,主è¦æ˜¯åŒ—美市场é“电缆å 比较多,而其他市场还是以铜为主)。

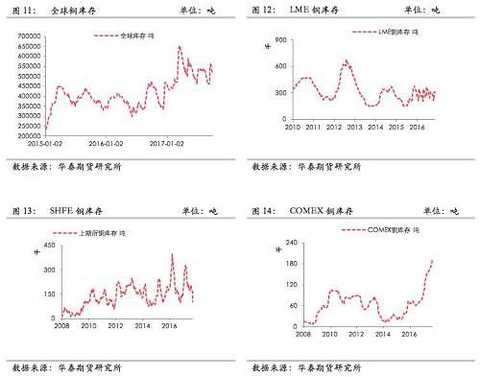

å…¨çƒé“œåº“å˜æƒ…况:

2017å¹´å‰ä¸‰ä¸ªå£åº¦ï¼Œå…¨çƒä¸‰å¤§äº¤æ˜“所库å˜ï¼ŒLME库å˜é™ä½Ž2.5万å¨ï¼ŒCOMEX库å˜å¢žåŠ 10.8万å¨ï¼ŒSHFE库å˜é™ä½Ž4.4万å¨ï¼Œå…¨çƒåº“å˜å‡€å¢žåŠ 3.9万å¨ã€‚

|

å…¨çƒé“œå¸‚场结论:

供应方é¢ï¼š

从9月跟踪情况æ¥çœ‹ï¼Œæ™ºåˆ©å’Œç§˜é²æœªæ¥äº§èƒ½å¢žåŠ 并ä¸æ˜¯ç‰¹åˆ«å¤šï¼Œæœªæ¥åå¹´æ™ºåˆ©é“œä¾›åº”å¢žåŠ ä¹Ÿä»…ä»…åœ¨110万å¨å·¦å³ï¼Œè€Œç§˜é²2021年之å‰çš„供应增é‡ä¹Ÿä»…在65万å¨å·¦å³ï¼Œæ™ºåˆ©å’Œç§˜é²çš„供应潜力真æ£é‡Šæ”¾å®žé™…上也ä¸æ˜¯å®¹æ˜“的事情,这æ„味ç€ï¼Œæœªæ¥é“œä¾›åº”很难集ä¸åˆ°æ¥ï¼Œä¾›åº”æ–¹é¢çš„压力并ä¸æ˜¯å¾ˆå¤§ã€‚

需求方é¢ï¼š

å…¨çƒé“œéœ€æ±‚å¯èƒ½ä¸å¤ªæœ‰è¶…过预期的情况。从我们对å三五需求估算的情况,2017å¹´ä¸å›½ç²¾ç‚¼é“œéœ€æ±‚增é‡æˆ–在30万å¨ï¼Œè€Œä¸‰å£åº¦è·Ÿè¸ªæƒ…况æ¥çœ‹ï¼Œå›½å®¶ç”µç½‘ä¾ç„¶ä»¥ç‰¹é«˜åŽ‹å»ºè®¾ä¸ºä¸»ï¼Œè€Œä¸å›½ä¹‹å¤–的需求目å‰ä¹Ÿæ²¡æœ‰å¤ªå¤§çš„潜力,整体需求以低速增长为主。

结论:

2017年预期全çƒä¾›åº”弹性ä¾ç„¶å˜åœ¨ï¼Œä¸è¿‡ï¼Œå¼¹æ€§åœ¨é™ä½Žï¼›ä½†æ˜¯éœ€æ±‚情况æ¥çœ‹ï¼Œæš‚时没有超预期的地方,如果以目å‰çš„需求能力,ä¸è¶³ä»¥ä½¿å¾—弹性消失,所以2017年铜供需整体宽æ¾ã€‚

ä¸è¿‡ï¼Œæœªæ¥å‡ 年供应的增é‡æ¯”è¾ƒä½Žï¼Œå› æ¤ï¼Œå¤§æ–¹å‘æ¥çœ‹ï¼Œé“œä¾›éœ€å‡ºçŽ°çŸç¼ºæ˜¯é«˜æ¦‚率事件,建议关注四å£åº¦å¯èƒ½å‡ºçŽ°çš„低å¸æœºä¼šã€‚æ•´ä½“ä¸Šï¼Œé“œä»·æ ¼æ˜¯ä¸€ä¸ªçœ‹é•¿åšçŸçš„过程。

ä¸å›½é“œå¸‚场供需:

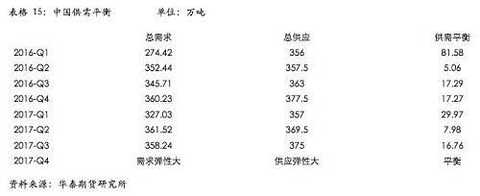

ä¸å›½é“œä¾›éœ€å¹³è¡¡çŽ°çŠ¶ï¼š

2017年三å£åº¦ï¼Œä¸å›½éœ€æ±‚åŒæ¯”整体å°å¹…å¢žåŠ ï¼Œä¸è¿‡ï¼Œä¾›åº”的弹性相对更大一些,使得整体三å£åº¦æ•´ä½“供需åå‘å°å¹…过剩。而四å£åº¦ï¼Œæ•´ä½“需求预估有一定的å£èŠ‚性好转,但是幅度å¯èƒ½ä¸ä¼šå¤ªå¤§ã€‚而四å£åº¦ç²¾ç‚¼é“œäº§èƒ½æœ‰ä¸€å®šæŠ•æ”¾ï¼Œä½†æ˜¯ä¾›åº”主è¦æ˜¯å—åˆ°é“œç²¾çŸ¿åŠ å·¥è´¹çš„é™åˆ¶ï¼Œæ•´ä½“供需基本上维æŒå¹³è¡¡çŠ¶æ€ã€‚

|

ä¸å›½é“œä¾›éœ€å¹³è¡¡å˜åŠ¨æ–¹å‘:

需求平稳:

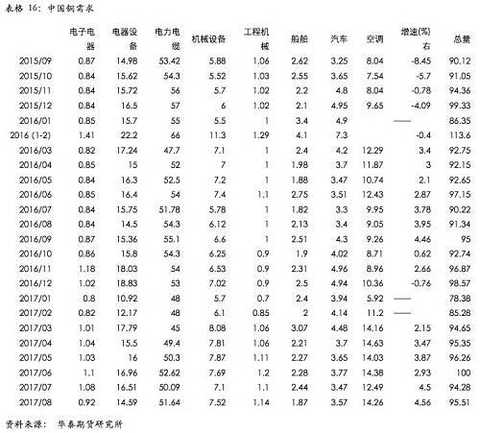

åŽæ³°æœŸè´§ç ”ç©¶æ‰€æ ¹æ®å›½å®¶ç»Ÿè®¡å±€æ•°æ®æµ‹ç®—,2017å¹´8月份,ä¸å›½é“œéœ€æ±‚整体上åŒæ¯”增速4.56%,环比增速å˜åŒ–ä¸å¤§ã€‚从增é‡æ¥æºæ¥çœ‹ï¼Œä¸»è¦æ˜¯ç©ºè°ƒé¢†åŸŸåŒæ¯”ä¾ç„¶æ¯”较强劲,电力电缆领域åŒæ¯”继ç»ä½Žè¿·ï¼Œä½†çŽ¯æ¯”有所好转。

而预计9月份,电力电缆领域环比继ç»æ”¹å–„,但是或难以和去年åŒæœŸç›¸æ¯”,空调领域åŒæ¯”æ•°æ®æˆ–继ç»è¡¨çŽ°è¾ƒå¥½ï¼Œä½†çŽ¯æ¯”å·²ç»è¿›å…¥å£èŠ‚性淡å£ã€‚

整体三å£åº¦éœ€æ±‚ä¿æŒæ¸©å’Œå¢žé•¿çš„æ ¼å±€ï¼Œè€Œå››å£åº¦å±•æœ›æ¥çœ‹ï¼Œå¢žé€Ÿéš¾ä»¥å‡ºçŽ°è¿‡äºŽæ¿€çƒˆçš„å˜åŒ–,整体ä¿æŒæ¸©å’Œå¢žåŠ çš„æ ¼å±€ï¼Œéœ€æ±‚æ–¹é¢è¾ƒä¸ºå¹³ç¨³ã€‚

|

|

电力电缆行业需求展望跟踪:

国家电力电网行业铜需求:

9月份,我们跟踪国家电网动å‘,情况如下:

特高压方é¢ï¼š

9月26日,2017å…¨çƒèƒ½æºäº’è”网高端论å›åœ¨äº¬å¬å¼€ï¼Œçºªå¿µä¹ 近平主å¸åœ¨2015å¹´9月26æ—¥è”åˆå›½å‘展峰会上,æ出的全çƒèƒ½æºäº’è”ç½‘å€¡è®®ä¸¤å‘¨å¹´ï¼ŒåŠ å¿«å…¨çƒèƒ½æºäº’è”网创新å‘展。

å…¨çƒèƒ½æºäº’è”网å‘展åˆä½œç»„织主å¸ã€ä¸å›½ç”µåŠ›ä¼ä¸šè”åˆä¼šç†äº‹é•¿åˆ˜æŒ¯äºšå‡ºå¸è®ºå›å¹¶ä½œä¸»æ—¨æ¼”讲。他表示,在ä¸å›½æ”¿åºœå’Œå›½é™…社会的大力支æŒä¸‹ï¼Œå…¨çƒèƒ½æºäº’è”网å‘展åˆä½œç»„织è”åˆå„方力é‡ï¼Œåœ¨ç†å¿µä¼ æ’ã€è§„åˆ’ç ”ç©¶ã€å›½é™…åˆä½œå’Œç»„织建设ç‰æ–¹é¢åšäº†å¤§é‡å·¥ä½œï¼ŒæŽ¨åŠ¨å…¨çƒèƒ½æºäº’è”网从战略构想进入共åŒè¡ŒåŠ¨çš„新阶段,开å¯äº†å…¨çƒèƒ½æºäº’è”网å‘å±•æ–°ç¯‡ç« ã€‚å…¨çƒèƒ½æºäº’è”网å‘展ä¸æ–实现新çªç ´ã€å¼€åˆ›æ–°å±€é¢ï¼Œå–得了显著æˆæ•ˆï¼Œèµ¢å¾—了广泛赞誉和å„方肯定。

å¦å¤–,9月åˆï¼Œå›½å®¶ç”µç½‘指出,国家电网公å¸â€œå…«äº¤ä¸ƒç›´â€å»ºè®¾æŠ•è¿ï¼Œâ€œäºŒäº¤å››ç›´â€æ£åœ¨å»ºè®¾ï¼Œ21æ¡ç‰¹é«˜åŽ‹å·¥ç¨‹å¦‚巨龙纵横东西å—北,输é€æ•°åƒä¸‡åƒç“¦çš„清æ´ç”µåŠ›ï¼Œä¸€å¼ 以特高压为骨干网架的åšå¼ºæ™ºèƒ½ç”µç½‘å·²ç»æˆå½¢ã€‚国家电网回顾了特高压的历å²ï¼Œç›®å‰å›½å†…属于大规模建设高峰时期,而未æ¥ï¼Œå¸ƒå±€å…¨çƒï¼Œå¸¦åŠ¨äº§ä¸šå‡çº§ï¼ŒåŠ 快“走出去â€ã€‚

结åˆå…¨çƒèƒ½æºäº’è”网化的战略,未æ¥ç‰¹é«˜åŽ‹ç”µç½‘ä¾ç„¶æ˜¯å›½å®¶ç”µç½‘的工作的é‡ç‚¹ã€‚

é…电网方é¢ï¼š

9月27日,从国家电网公å¸ä¸‰å£åº¦æ–°é—»å‘布会上获悉,ç»è¿‡ä¸€å¹´åŠçš„艰苦奋战,公å¸å…‹æœæ—¶é—´ç´§ã€ä»»åŠ¡é‡ã€æ–½å·¥éš¾åº¦å¤§ç‰å›°éš¾ï¼Œå‘¨å¯†éƒ¨ç½²ã€ç²¾å¿ƒç»„织ã€ä¸¥æ ¼ç®¡ç†ï¼ŒäºŽ9月25æ—¥æå‰ä¸‰ä¸ªæœˆå®Œæˆæ–°ä¸€è½®å†œç½‘æ”¹é€ å‡çº§â€œä¸¤å¹´æ”»åšæˆ˜â€ã€‚æ–°é—»å‘布会上,公å¸æ–°é—»å‘言人å‘媒体和社会å‘布了公å¸åšå†³è´¯å½»å…šä¸å¤®ã€å›½åŠ¡é™¢å†³ç–部署,切实履行央ä¼â€œä¸‰å¤§è´£ä»»â€ã€è·µè¡Œâ€œå…个力é‡â€ï¼Œå…¨åŠ›æŽ¨è¿›å†œç½‘工程建设,切实åšå¥½ä¾›ç”µæœåŠ¡å·¥ä½œæƒ…况。公å¸ç´¯è®¡æŠ•èµ„1423.6亿元,完æˆäº†ç»è¥åŒºå†…153.5万眼平原地区农田机井通电,实现了平原地区“井井通电â€ç›®æ ‡ï¼›å®žçŽ°äº†6.6万个å°åŸŽé•‡ï¼ˆä¸å¿ƒæ‘ï¼‰ç”µç½‘æ”¹é€ å‡çº§å…¨è¦†ç›–;完æˆäº†7.8万个自然æ‘新通动力电åŠæ”¹é€ ,实现æ‘æ‘é€šåŠ¨åŠ›ç”µç›®æ ‡ï¼Œå—益人å£è¾¾1.56亿人。通过这些工程的实施,国家电网公å¸ç»è¥åŒºåŸŸå†…农æ‘地区供电能力和æœåŠ¡æ°´å¹³æ˜Žæ˜¾æå‡ï¼Œæ–°æ”¹é€ æ‘镇户å‡é…å˜å®¹é‡æ高到2.64åƒä¼å®‰ï¼Œä¾›ç”µèƒ½åŠ›æå‡65%,农网供电å¯é 率和综åˆç”µåŽ‹åˆæ ¼çŽ‡åˆ†åˆ«è¾¾åˆ°99.808%ã€99.677%。

æ ¹æ®å›½åŠ¡é™¢éƒ¨ç½²ï¼Œå›½å®¶ç”µç½‘å…¬å¸æ–°ä¸€è½®å†œç½‘æ”¹é€ å‡çº§å·¥ç¨‹è§„划总投资5222亿元,工程总体5年完æˆï¼Œä¸»è¦åŒ…括“井井通电â€å·¥ç¨‹ï¼Œå°åŸŽé•‡ï¼ˆä¸å¿ƒæ‘ï¼‰ç”µç½‘æ”¹é€ å‡çº§ï¼Œæ‘æ‘通动力电,光ä¼æ‰¶è´«é¡¹ç›®æŽ¥ç½‘工程,西部åŠè´«å›°åœ°åŒºå†œç½‘供电æœåŠ¡å‡ç‰åŒ–,东ä¸éƒ¨åœ°åŒºåŸŽä¹¡ç”µç½‘一体化,西è—ã€æ–°ç–†ä»¥åŠå››å·ã€ç”˜è‚ƒã€é’æµ·3çœè—区农æ‘电网建设ç‰7项工程。其ä¸ï¼Œå‰ä¸‰é¡¹å·¥ç¨‹æ˜¯å›½å®¶å®‰æŽ’çš„å‰ä¸¤å¹´é‡ç‚¹å»ºè®¾ä»»åŠ¡ï¼Œ2016å¹´å¯åŠ¨ï¼ŒåŽŸè®¡åˆ’2017年年底完æˆã€‚å‘布会还å‘布了公å¸æŽ¨è¿›æ¸¯å£å²¸ç”µåŠç”µèƒ½æ›¿ä»£æ•´ä½“工作情况。近年æ¥ï¼Œå…¬å¸åœ¨å±…民采暖ã€å·¥å†œä¸šç”Ÿäº§åˆ¶é€ ã€äº¤é€šè¿è¾“ã€ç”µåŠ›ä¾›åº”与消费ã€å®¶åºç”µæ°”化ç‰é‡ç‚¹é¢†åŸŸï¼Œå¤§åŠ›æŽ¨å¹¿æ¸…æ´å–æš–ã€ç…¤æ”¹ç”µã€æ¸¯å£å²¸ç”µç‰æ›¿ä»£æŠ€æœ¯ï¼Œé™†ç»å»ºæˆä¸€å¤§æ‰¹å…¸åž‹ç¤ºèŒƒé¡¹ç›®ã€‚截至8月底,累计推广实施电能替代项目9万余个,完æˆæ›¿ä»£ç”µé‡è¿‘3200亿åƒç“¦æ—¶ï¼ŒæŽ¨åŠ¨ç¤¾ä¼šç”¨èƒ½ä¸Žç”Ÿäº§ç”Ÿæ´»æ–¹å¼å‘生é‡è¦å˜åŒ–,å–得了良好社会效益和ç»æµŽæ•ˆç›Šã€‚å‘布会还å‘布,2018年年底,京æ大è¿æ²³æ°´ä¸Šå…¬å…±æœåŠ¡åŒºå°†å®žçŽ°ç»¿è‰²å²¸ç”µå…¨è¦†ç›–。

整体上,æ¤å‰ä¸€è½®å†œæ‘电网集ä¸æ”¹é€ å·²ç»ç»“æŸï¼Œæœªæ¥é…电网建设集ä¸åœ¨è¥¿åŒ—和西å—地区,这也是æ¤å‰è°ƒç ”ä¸ï¼Œè¥¿åŒ—和西å—地区电力电缆ä¼ä¸šè®¢å•æƒ…况较好的主è¦åŽŸå› 。

民用电缆电线领域:

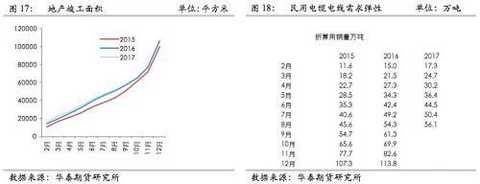

尽管房地产增速放缓,但是在民用电缆电线领域,åŽæœŸéœ€æ±‚展望主è¦åœ¨äºŽæ¶ˆè´¹çš„çœçº§ï¼Œå¦‚果按照4平方毫米和多线路的平å‡å¸ƒçº¿ï¼Œæˆ‘们计算的房屋竣工é¢ç§¯åŽæœŸå¯ä»¥å¸¦æ¥çš„需求也是å¯ä»¥å€¼å¾—期待的。

|

空调行业需求展望跟踪:

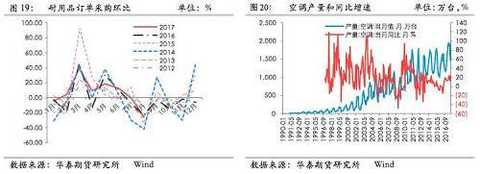

å‰ä¸‰å£åº¦ï¼Œç©ºè°ƒäº§é‡ç»´æŒè¾ƒé«˜çš„åŒæ¯”增速,ä¸è¿‡ï¼Œç¬¬ä¸‰å£åº¦ï¼Œå› å£èŠ‚æ€§å› ç´ ï¼Œç©ºè°ƒè¡Œä¸šçŽ¯æ¯”æ•°æ®å·²ç»ä¸‹é™ï¼Œä½†åŒæ¯”ä¾ç„¶ç»´æŒè¾ƒé«˜å¢žé€Ÿã€‚

|

ä¸å›½é“œä¾›åº”:

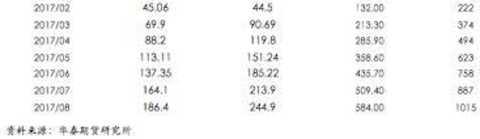

ä¸å›½é“œä¾›åº”现状:1-8月总供应åŒæ¯”有所扩å¼

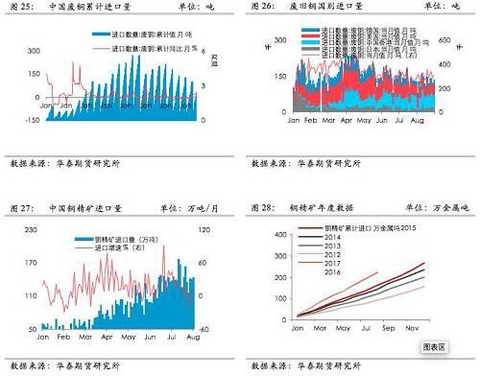

2017å¹´1-8月,从直接å£å¾„统计的ä¸å›½é“œæ€»ä¾›åº”é‡ä¸º1015万å¨é™„近,å°å¹…高于去年åŒæœŸçš„988万å¨ï¼Œå…¶ä¸ï¼Œç²¾ç‚¼é“œè¿›å£186万å¨ï¼Œå¤§å¹…度低于去年åŒæœŸçš„222.5万å¨ã€‚精炼铜产é‡åˆ™ä»ŽåŽ»å¹´åŒæœŸçš„549万å¨å¢žåŠ 至584万å¨ï¼Œå¦å¤–废旧铜进å£ä¹Ÿä»Ž215.8万å¨å¢žåŠ 至245万å¨ã€‚å¦å¤–,8月份,ä¸å›½æ€»ä¾›åº”大约在125万å¨é™„近,而预估,9æœˆä»½æ•´ä½“ä¾›åº”é¢„ä¼°çŽ¯æ¯”å¢žåŠ æœ‰é™ï¼ŒçŽ¯æ¯”或æŒå¹³ã€‚

å¦å¤–,四å£åº¦å±•æœ›ä¸Šï¼Œå°½ç®¡å››å£åº¦é¢„ä¼°ä»ç„¶æœ‰ç²¾ç‚¼äº§èƒ½æŠ•æ”¾ï¼Œä½†æ˜¯åŠ 工费采è´åº•çº¿è¾ƒé«˜ï¼Œå®žé™…精炼铜产é‡ä¾ç„¶å—åˆ°æŠ‘åˆ¶ã€‚å› æ¤ï¼Œå›½å†…总供应的扩大或é‡æ–°éœ€è¦è¿›å£ï¼Œå› æ¤ï¼Œè¿›å£ç›ˆäºæˆ–ä¿æŒåœ¨è¾ƒå¥½çš„ä½ç½®ã€‚

|

|

而从间接å£å¾„æ¥çœ‹ï¼Œ1-8月份铜精矿和废旧铜进å£åŒæ¯”å‡ç»§ç»å¢žåŠ ,精炼铜进å£çš„缩å‡å¹…度é™ä½Žï¼Œæ•´ä½“1-8月份总供应åŒæ¯”æœ‰æ‰€å¢žåŠ ã€‚è€Œé¢„è®¡å››å£åº¦ï¼Œæ€»ä¾›åº”或ä¿æŒåŒæ¯”å°å¹…å¢žåŠ çš„æ ¼å±€ã€‚

|

|

ä¸å›½é“œæ€»ä¾›åº”展望:增é‡å¼¹æ€§æˆ–在四å£åº¦é‡Šæ”¾å®Œæ¯•

ä¸å›½ç²¾ç‚¼é“œäº§é‡åŒæ¯”继ç»ç»´æŒå¢žé•¿ï¼Œä¸è¿‡ï¼ŒçŽ¯æ¯”å˜åŒ–并ä¸æ˜¯å¾ˆå¤§ï¼Œè™½ç„¶é¢„估精炼铜产能继ç»æŠ•æ”¾ï¼Œä½†æ˜¯å—é™åŠ 工费,精炼铜实际增é‡é¢„估有é™ï¼›å¦å¤–,å—到国内质é‡æŽ§åˆ¶çš„é™åˆ¶ï¼ŒåºŸæ—§é“œè¿›å£æˆ–å—到抑制,å¦å¤–,精炼铜进å£éœ€è¦è¾ƒå¥½çš„比价,整体供应弹性ä¸æ˜¯å¾ˆå¤§ã€‚

|

|

ä¸å›½é“œä¾›éœ€å¹³è¡¡ç»“论

需求:

åŽæ³°é“œç ”究å°ç»„æ ¹æ®å三五规划数æ®è®¡ç®—æ ¸å®žï¼Œå三五期间,ä¸å›½ç²¾ç‚¼é“œéœ€æ±‚å¹³å‡å¢žé‡æˆ–在30万å¨/年。

三å£åº¦ï¼Œæ•´ä½“铜需求维æŒä½Žé€Ÿå¢žåŠ ,从三å£åº¦çš„跟踪的情况æ¥çœ‹ï¼Œå›½å®¶ç”µç½‘å·²ç»å®Œæˆå†œæ‘ç”µç½‘æ”¹é€ ï¼Œæœªæ¥ç”µç½‘建设主è¦ä¾èµ–西å—ã€è¥¿åŒ—åœ°åŒºç”µç½‘æ”¹é€ ï¼Œä½†æ˜¯æ—¶é—´ç›¸å¯¹ç¼“æ…¢ï¼Œæ•´ä½“éœ€æ±‚ä¾ç„¶æ³¢æ¾œä¸æƒŠã€‚

供应:

三å£åº¦ï¼Œä¸å›½é“œæ€»ä¾›åº”两个å£å¾„统计åŒæ¯”开会æ¢å¤å¢žåŠ ,主è¦æ˜¯ç²¾ç‚¼é“œè¿›å£å‡å°‘有所缓和;四å£åº¦ï¼Œå›½å†…精炼铜产能继ç»æŠ•æ”¾ï¼Œä½†æ˜¯é“œç²¾çŸ¿åŠ 工费或低于冶炼ä¼ä¸šé‡‡è´åº•çº¿ï¼Œå› æ¤ï¼Œæ•´ä½“供应压力比较有é™ã€‚

结论:

综åˆæ¥çœ‹ï¼Œé“œéœ€æ±‚整体ä¿æŒä½Žé€Ÿå¢žé•¿ï¼Œè€Œå›½å†…精炼铜供应继ç»å—åˆ°é“œç²¾çŸ¿åŠ å·¥è´¹çš„å›°æ‰°ï¼Œç²¾ç‚¼äº§èƒ½æŠ•æ”¾æœªå¿…ä¸€å®šèƒ½å¤Ÿå¸¦æ¥ç²¾ç‚¼é“œä¾›åº”çš„å¢žåŠ ï¼Œæ•´ä½“ä¾›éœ€åŸºæœ¬å¹³è¡¡ã€‚

作者: å´ç›¸é”‹

æ¥æºï¼šåŽæ³°æœŸè´§ç ”究院

Enter [Sina Finance and Economics Unit] Discussion

Down jackets are usually filled with materials such as feathers and goose down, which provide warmth when worn. Therefore, down jackets are suitable for wearing in cold winters and do not feel cold compared to thin coats. Moreover, there are many styles of down jackets available, suitable for most adult women to wear. Women can choose according to their own needs. According to customer feedback, they feel warm when wearing them.

Ladies Down Jacket ,Red Puffer Jacket Women,Ladies Long Puffer Coat,Ladies Puffer Coat

T&H INTERNATIONAL TRADING LIMITED , https://www.th-shoetrend.com